More Related Content Similar to Assessment guide AFAQ 26000 Similar to Assessment guide AFAQ 26000 (20) More from Groupe AFNOR (20) 1. E N T E R P R I S E S / O R G A N I Z AT I O N S

Assessment Guide AFAQ 26000

Sustainable Development

Corporate Social Responsibility

Human Environmental

AFAQ Production

and consumer

Resources

results

26000

Regional

protection

roots

Social

CORPORATE SOCIAL Strategy and results

corporate

RESPONSIBILITY Approach social

responsibility

Economic

results

2. Human Environmental

AFAQ Production

and consumer

Resources

results

26000

Regional

protection

roots

Social

CORPORATE SOCIAL Strategy and results

corporate

RESPONSIBILITY Approach social

responsibility

Economic

results

2 Assessment Guide AFAQ 26000 - Enterprises / Organizations

© Any integral or partial reproduction, made apart from an authorization express of AFNOR Certification or of its having causes, is illicit.

3. Preface

W

hatever the sector, it has become almost indispensable for companies, and organisa-

tions in general, to position themselves in terms of sustainable development. What fac-

tors legitimise their activities, products or services? What is their ability to create value

sustainably while meeting their stakeholders’ expectations?

Organisations are thus increasingly required to account for their contribution to sustainable

development and their ability to attain an overall level of performance, balanced on three pillars

: economic, social and environmental.

2010 is a historic milestone, both for voluntary regulation tools on an international level, including

standardisation, and for Corporate Social Responsibility (CSR).

Indeed, the publication on 1st November of ISO 26000, the first international CSR Guidelines,

offers a common definition for the first time, enabling such responsibilities to be clearly deline-

ated and exercised.

‘Corporate Social Responsibility’ refers to the contribution made by organisations to sustain-

able development. ISO 26000 explores and develops these concepts and sets strong bench-

marks, both in terms of resources and underlying tenets, by means of 7 core CSR subjects and

7 CSR Principles. The standard implicates both the strategic thinking and the methods of an

organisation—as well as its means, goals and its operational deployment of Corporate Social

Responsibility.

ISO 26000 also takes account of the fact that each organisation’s CSR solutions are unique: they

depend on their sector, context and culture, in a changing world where knowledge, innovation

and stakeholder expectations continually influence the state of the art of CSR practices.

ISO 26000 also reiterates an element that was an integral part of the mandate granted to

the experts and stakeholders involved in its development: this standard is not intended for

certification.

It is in order therefore to help organisations assess the relevance and maturity level of their prac-

tices (in a spirit of assessment rather than certification), that over the last three years, AFNOR

Certification and the AFNOR Group have acquired unique insights into evaluating the extent to

which organisations practise sustainable development. Our methods and expertise have thus

proved their robustness and added value, irrespective of sector or size of organisations.

AFNOR Certification is thus more than ever ready to work alongside all organisations—from the

smallest to the largest—that wish to assess, demonstrate, seek recognition of and improve their

approach to Corporate Social Responsibility.

Florence Méaux, General Manager

Assessment Guide AFAQ 26000 - Enterprises / Organizations 3

© Any integral or partial reproduction, made apart from an authorization express of AFNOR Certification or of its having causes, is illicit.

4. Human Environmental

AFAQ Production

and consumer

Resources

results

26000

Regional

protection

roots

Social

CORPORATE SOCIAL Strategy and results

corporate

RESPONSIBILITY Approach social

responsibility

Economic

results

Preamble

I

n 1987 the United Nations World Commission on Environment and Development, known as

the Brundtland Commission, introduced and defined the concept of sustainable development

as «development that meets the needs of the present without compromising the ability of

future generations to meet their own needs».

The various stakeholders attending the UN Rio Summit in 1992 (NGOs, states, local govern-

ments, unions, companies) seized on the issue with enthusiasm.

Events in recent years have brought concerns and issues related to sustainable development to

the forefront, on a worldwide scale, with climate negotiations, mobilisation on biodiversity, the

Millennium Goals, the raising issues of the social conditions of workers globally, and so forth.

In this context, Corporate Social Responsibility, defined as «the voluntary contribution of organi-

sations to sustainable development», offers a framework and an opportunity for organisations—

and particularly for businesses—to demonstrate their uptake of social and environmental issues

in conjunction with their stakeholders.

The year 2010 marks a historic milestone, both for sustainable development, international nego-

tiations within the ISO (the International Organization for Standardization) and CSR. Indeed, with

the publication on 1st November, of ISO 26000: International Guidelines for Corporate Social

Responsibility, actors worldwide have, for the first time, a common frame of reference with which

to define and implement CSR.

ISO 26000 calls for the formulation of CSR strategy in tandem with the global challenges of sus-

tainable development and a given organisation’s characteristics, constraints and opportunities.

ISO 26000 provides the keys and makes linkages with the tools, including control mechanisms

(indicators...) with which to build, invigorate and improve this process.

The approach to social responsibility of each organisation and business is unique and requires

responses and practices based on its own issues, context and culture. ISO 26000 stresses this

point and makes no a priori requirements.

Organisations are invited to measure the soundness of their practices, and these, where appli-

cable, deserve to be acknowledged, valued and communicated. Responsible organisations also

deserve to be distinguished from the advertising practices and “greenwashing” carried out by

actors who occasionally knowingly misrepresent their contribution to sustainable development.

It is therefore natural to raise

the question of evaluating ISO

26000 compliance as a tool for

reflection, steering and external

dialogue. Based on the expertise and experience in

Sustainable Development issues of the AFNOR

Group, AFNOR Certification has developed

a methodology for evaluating the ISO

26000 compliance of organisations:

AFAQ 26000

4 Assessment Guide AFAQ 26000 - Enterprises / Organizations

© Any integral or partial reproduction, made apart from an authorization express of AFNOR Certification or of its having causes, is illicit.

5. Contents

Introduction............................................................................................... 6

Assess your Corporate Social Responsibility today. ........................ 7

.

and pave the way for tomorrow

The assessment process......................................................... 8

The AFAQ 26000 Model: General remarks......................... 11

1. Practices...................................................................................... 12

Criterion 1 Vision of CSR

& Governance................................................................................ 12

.

Criterion 2 Implementation: Integration

and communication of CSR......................................................... 14

Criterion 3 Human resources,

labour relations and practices...................................................... 16

Criterion 4 Modes of production, sustainable

consumption and consumer issues............................................. 18

Criterion 5 Local integration: communities

and local development.................................................................20

2. Results......................................................................................21

Pilier 6 : Environmental results........................................................21

Pilier 7 : Social results.......................................................................22

Pilier 8 : Economic results.................................................................. 24

The AFAQ 26000 Model: Assessment principles.................. 25

Recognition valid for up to 3 years. ........................................... 28

.

The expertise and skills of evaluators............................................... 30

Glossary...................................................................................................... 31

Assessment Guide AFAQ 26000 - Enterprises / Organizations 5

© Any integral or partial reproduction, made apart from an authorization express of AFNOR Certification or of its having causes, is illicit.

6. Human Environmental

AFAQ Production

and consumer

Resources

results

26000

Regional

protection

roots

Social

CORPORATE SOCIAL Strategy and results

corporate

RESPONSIBILITY Approach social

responsibility

Economic

results

Introduction

AFAQ 26000, building on AFAQ 1000NR

3 years of progress and lessons learned

I

n 2007, AFNOR Certification developed an assess- A mixture of businesses, non-profit organisations, trade

ment approach of the way organisations incorporate unions etc. of all sizes and in all sectors have worked

sustainable development into their strategies, man- with us as pioneers in the field. Over a hundred inno-

agement and results: AFAQ 1000NR. vative organisations committed to sustainable devel-

opment (whether as a recent initiative on their part or

It was an innovative strategic choice. By including actors a mature policy), have called upon our experts to take

who were themselves expert in sustainable development the temperature of their Corporate Social Responsibility

(having participated in the major summits as well as the policy, share our findings with their internal and exter-

most innovative methodological developments of recent nal stakeholders, and identify ways forward to further

years: SD 21000 etc...), AFNOR Certification made develop their strategies and practices with a view to bet-

a choice to invest in the processes and competences ter overall performance.

of corporate social responsibility, in anticipation of the

release of ISO 26000. Large companies, entities operating within such compa-

nies, medium, small and very small businesses (includ-

Since the beginning of international work on ISO 26000, ing some with fewer than 10 employees), in the sectors of

the mandate of the Standardisation Commission had energy, food, services, building and public works, land-

been clear: this would be a new type of standard (a scape, social housing, and many more, have contributed

«standard of conduct»), which would neither aim to out- over the past three years to making first AFAQ 1000NR

line requirements in terms of a management system, then AFAQ 26000 France’s leading provider of sustaina-

nor to become a certifiable framework (the preamble to ble development practice assessment1. Our clients both

ISO 26000 explicitly emphasises this stance). in France and abroad have shown confidence both in our

original methodology and in the men and women whose

Indeed, the relevant practices deployed by each organi- expertise undergirds our approach.

sation are different and organic and cannot be prede-

fined in advance. According to locations, activities, AFNOR Certification has acquired and consolidated the

cultures, practices and available technologies, and on expertise of a dedicated pool of evaluators pooling their

stakeholders’ changing circumstances, challenges and CSR assessment practices. These evaluators are quali-

expectations, Corporate Social Responsibility consists fied experts and their skills are continuously refreshed

precisely of identifying and deploying appropriate prac- and updated, adding even more value for our customers

tices and improving and revising these over time. in terms of their current questions about the future.

In this context, in order to ascertain uptake of ISO 26000 The enthusiasm of our customers and the course of

issues and principles by organisations, the AFNOR international events have more than justified our choices.

Group, in line with the recommendations of ISO, consid-

ers assessment to be the most relevant methodology, in Make your commitment count with us and join the family

both ethical and technical terms, for all matters relating of globally responsible organisations.

to corporate social responsibility.

AFNOR Certification now has 3 years’ experience of

evaluating the contribution of organisations to sustain-

able development, thanks to AFAQ 1000NR, which was

already in line with ISO 26000.

1. Not counting companies quoted on the stock exchange.

6 Assessment Guide AFAQ 26000 - Enterprises / Organizations

© Any integral or partial reproduction, made apart from an authorization express of AFNOR Certification or of its having causes, is illicit.

7. Assess your Corporate Social

Responsibility today and pave the way

for tomorrow

AFAQ 26000, assess your Corporate Social development: ISO 26000, the Rio Declaration, Global

Responsibility Reporting Initiative, Global Compact, SD21000...

n external assessment which defines and implements

A AFAQ 26000: Enrich your relationship with

ISO 26000 stakeholders

Abalanced measure of your organisation’s strategic,

managerial and operational behaviour, practices and

nalysis

A and integration of stakeholder expectations:

the assessment includes interviews with various stake-

outcomes

holders (employees, health and safety committees,

rating scale of 1000 points that represents four matu-

A customers, suppliers, partners etc.)

rity levels: Initial, Progression, Confirmed, Exemplary

upport

S for stakeholder dialogue through the

xpert

E CSR assessors, qualified and trained within Assessment Report

a dedicated pool, with several years of experience in

most sectors

pening

O up to new stakeholders and improving local

integration.

A summary Assessment Report—a real tool for strategic

and operational management, offering suggestions for

improvement.

AFAQ 26000: Develop and strengthen your

business

AFAQ 26000: Enhance your contribution to sus- truly international passport testifying to your organi-

A

tainable development sation’s CSR achievements

ommunicate your level of performance: a recognised

C evelopment of new markets or products

D

and communicable Assessment Certificate and Logo, reas for improvement: reduction of energy costs and

A

from Progress Level onwards raw materials, security of supply channels, choice of

nsure

E the loyalty of your customers and other alternative means of transport...

stakeholders through your commitment to social

responsibility. AFAQ 26000: an optimised service

everage

L your actions and your external stakehold- n

A assessment covering all sustainable development

ers (employees, shareholders, partners, customers, issues throughout the organisation (or within a coher-

suppliers...) ent area).

ain easier access to markets

G Strategic, managerial and operational practices

mprove your awareness and reputation

I (strategy, management, HR, production methods,

local integration)

AFAQ 26000, an approach adapted to your con- Competency in managing performance in terms

text and your strategy of Corporate Social Responsibility (environmental,

social, and economic outcomes)

uitable for all kind of organisations (large companies

S ptimised 3-phase process

O

and subsidiaries, SMEs, very small businesses, local

authorities and governments) and sectors

elivered by AFNOR Certification,

D the organisations

assessment specialists: our optimised value-for-

seful

U at all stages of the process: from simple money service delivers strong strategic and opera-

inventory to leveraging previous endeavours by your tional added value.

organisation

onsistent with the main reference texts on sustainable

C

Assessment Guide AFAQ 26000 - Enterprises / Organizations 7

© Any integral or partial reproduction, made apart from an authorization express of AFNOR Certification or of its having causes, is illicit.

8. Human Environmental

AFAQ Production

and consumer

Resources

results

26000

Regional

protection

roots

Social

CORPORATE SOCIAL Strategy and results

corporate

RESPONSIBILITY Approach social

responsibility

Economic

results

assessment process

AFAQ 26000

The assessment approach

The assessment follows a clear approach: to demonstrate the capacity of the entity being

assessed to appropriately identify its CSR issues, deploy relevant operational and managerial

practices and manage results so as to improve its overall performance (in line with stakeholder

expectations).

Objective:

To demonstrate that the organisation’s

strategy and practices facilitate the

attainment of positive results in various

aspects of sustainable development.

Focus of conclusions: On-site assessment

T

he maturity level of strategy of the extent to which the business

and practices has integrated CSR

T

he capacity to manage and achieve

key outcomes

C

ausal linkages between practices

and results.

Given the comprehensiveness of the AFAQ 26000 model and the diversity of CSR issues, assess-

ment is conducted by pairs of assessors, except for organisations of fewer than 50 employees

(in which a narrower pool of dedicated assessors is qualified to intervene).

Assessment phases

The assessment service is conducted in 3 main phases:

n and off-site preparation

O

n-site implementation

O

n and off-site analysis

O

8 Assessment Guide AFAQ 26000 - Enterprises / Organizations

© Any integral or partial reproduction, made apart from an authorization express of AFNOR Certification or of its having causes, is illicit.

9. The different phases of an AFAQ 26000 assessment

The main objectives of the three phrases are outlined in the diagram below:

1 2 3

Partial on-site On-site assessment Partial on-site

preparation analysis

D

ata gathering: D

ata gathering in terms of D

rafting of Assessment

Documentary review and approaches, practices and Report

identification of diverse results via interviews with A

warding of overall score,

indicators specified managers, staff identification of practices to

I

dentification of and stakeholders and related be continued and areas for

stakeholders to be met documentary analysis improvement (during final

(including 5 external M

ulti-site consolidation debriefing meeting)

stakeholders) where necessary, depending P

resentation of Assessment

D

rafting of assessment on context Certificate containing score

plan, including meetings with O

ptional facilitation of focus and relevant level, and

specified stakeholders groups: assessment and presentation of associated

I

nitial data analysis collective sharing of CSR logo

practices

On-site preparation con- mprove and manage communication with internal and/

I

1 tributes to a large extent

to the added value of an

AFAQ 26000 assessment.

or external stakeholders (based on the Assessment

Report...)

Partial on-site ..

.

preparation The assessment aims are

identified and clarified in

Preparation, in conjunction with the management of the

conjunction with manage-

entity being evaluated, can help define the terms most

ment.

relevant for evaluating its practices and management

tools, leading to an assessment plan incorporating the

These aims can be on different levels and are often com-

various stakeholders, both internal and external, to be

plementary:

contacted.

stablish a reliable barometer via a third party assess-

E

ment of the organisation’s integration of Corporate On-site preparation takes place ahead of the assess-

Social Responsibility ment proper. This advance data-gathering exercise

rovide an external perspective and expertise through-

P enables the entity being evaluated to outline the benefits

out the entity being evaluated, highlighting practices to it expects from the analysis of its practices, manage-

be continued and its areas for improvement. Identify ment and outcomes.

action plans based on priorities Such a clarification, a learning experience for the entity

acilitate awareness of required changes via an out-

F being evaluated, helps the evaluator to identify the enti-

side perspective; ty’s key characteristics and issues.

The data required for the preparation of the assessment

stablish a system of internal or external comparison

E

include:

(benchmarks) for practices and outcomes

he entity’s policy and strategy

T

repare for sustainable development awards

P

eneral information about the entity (relationship

G

emonstrate commitment to Sustainable Development

D with a group, organigram, presentation literature and

and Corporate Social Responsibility to clients, pros- description of activity, etc.)

pects, and other stakeholders

Assessment Guide AFAQ 26000 - Enterprises / Organizations 9

© Any integral or partial reproduction, made apart from an authorization express of AFNOR Certification or of its having causes, is illicit.

10. Human Environmental

AFAQ Production

and consumer

Resources

results

26000

Regional

protection

roots

Social

CORPORATE SOCIAL Strategy and results

corporate

RESPONSIBILITY Approach social

responsibility

Economic

results

he set of indicators to be monitored by the entity (the

T to the business and its location(s) be contacted (cli-

results must usually cover a sufficient period to indi- ents, suppliers, regional industry, research and envi-

cate a trend) ronment officials [DRIRE], occupational health officers,

arious documents relating to management (process

V local authority environment and energy management

mapping where applicable, records relating to internal authorities, residents’ associations, labour market

and external communication on the subject...) integration associations, training networks, fire-fight-

… ers, prefecture...). These stakeholders are contacted

either by phone or met during the on-site assessment

Identification of stakeholders to be contacted dur- (e.g. during a working lunch).

ing the assessment takes place directly with the entity’s

management and consists of two steps: The preparation also enables us, in conjunction with

. Identification of internal staff and stakeholders: all

1 the management team, to consider the details of the

managers (financial, human resources,...), employees debriefing, identifying the target audience for delivery

and their representatives (shop stewards, HSC mem- of the assessment conclusions. A further more com-

bers…), shareholders; face-to-face meetings take plete debriefing (including all the scores by practice and

place with these stakeholders during the assessment results), before a select audience (management commit-

as agreed in the assessment plan. tee, all staff, external stakeholders...) is also an option,

depending on the objectives pursued by the leaders of

. Identification of external stakeholders: it is recom-

2

entity being assessed.

mended that at least 5 external stakeholders relevant

2 3

On-site assessment Analysis: the

Assessment and

Debriefing Report

The evaluator factually analyses good practices to be

continued and areas for improvement, so as to be able The evaluator may make use of an off-site period for

to record a score for each sub-criterion in the practice writing the assessment report, consolidating the overall

assessment model. score and preparing the debriefing meeting.

During assessment, various employees of the entity During the debriefing meeting, the evaluator presents the

being evaluated may be interviewed, as well as various organisation’s strengths and areas for improvement for

external stakeholders identified during the preparation, the 5 practice criteria and 3 results criteria.

in order to gather factual examples which can feed into The overall score and the level attained are also com-

planning, implementation, deployment, measurement municated.

and improvement of practices covered by the AFAQ

26000 model. Then, against each criterion, s/he debriefs on the salient

The evaluator also assesses the relevance of given indi- facts characterising the company’s approach and matu-

cators in relation to the issues and the attainment lev- rity level in terms of Corporate Social Responsibility.

els of objectives, trends and comparisons with external

data, in order to determine the score assigned to out- The evaluator factors in the exchanges of views and

comes sub-criteria of the AFAQ 26000 model. comments made by the organisation during the debrief-

ing meeting in the final drafting of the assessment report.

As the assessment takes place over several days, the

assessor may call interim review meetings to present S/he completes the assessment report and sends it to

material collected in order to clarify any ambiguities and the chargé d’affaires. The assessment report is then for-

facilitate the debriefing meeting. warded by the chargé d’affaires to the assessed entity.

10 Assessment Guide AFAQ 26000 - Enterprises / Organizations

© Any integral or partial reproduction, made apart from an authorization express of AFNOR Certification or of its having causes, is illicit.

11. The AFAQ 26000 Model

AFAQ 26000 was developed in line

with key benchmarks for sustainable

development: SD21000, GRI, the Human Environmental

Resources

Global Compact, the UN Agenda 21,

Production

results

and of course the entire contents of

and consumer Regional

the ISO 26000. protection roots

Social

CORPORATE SOCIAL Strategy and results

corporate

RESPONSIBILITY Approach social

responsibilit

Economic

results

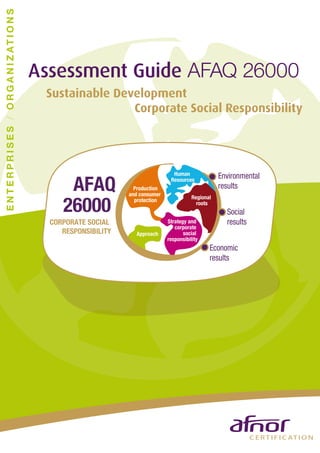

AFAQ 26000, a model for assessing the integration of Corporate Social Responsibility strategy and practices by

organisations, focuses on two types of assessment:

Assessment of strategic, managerial Assessment of results

and operational practices

relative to the 3 pillars of sustainable development:

This involves assessing the maturity of practices in terms This involves assessing the organisation’s ability to iden-

of Corporate Social Responsibility throughout the follow- tify and manage indicators relevant to its challenges,

ing criteria: against the following three criteria:

1 Vision in terms of CSR Governance 6

Environmental results

2

Implementation: the integration 7

Social results

and communication of CSR

8

Economic results

3

Human resources, labour relations and practices

4

Modes of production, consumption The assessors seek to establish causal links between

and consumer issues practices and results.

Moreover, each of these three criteria includes a sub-

5

Local integration: communities and local criterion of ability to monitor stakeholder satisfaction

development relative to (environmental, social and economic) expec-

tations and impact.

Each of these criteria consists of several sub-criteria to

be analysed and assessed. The sub-criteria incorporate

and implement the content of ISO 26000.

Assessment Guide AFAQ 26000 - Enterprises / Organizations 11

© Any integral or partial reproduction, made apart from an authorization express of AFNOR Certification or of its having causes, is illicit.

12. Human Environmental

AFAQ Production

and consumer

Resources

results

26000

Regional

protection

roots

Social

CORPORATE SOCIAL Strategy and results

corporate

RESPONSIBILITY Approach social

responsibility

Economic

results

1. Practices

The aim of this section is to review the criteria and sub-criteria for strategic, managerial and

operational practices under the AFAQ 26000 model.

Criterion 1 Vision of CSR Governance

This is the core criterion of the AFAQ 26000 assessment which addresses them in a comprehensive and contex-

model. The evaluator seeks to assess the vision, strategy tualised way.

and governance of the approach to corporate social

responsibility, consistent with the key concepts of ISO Indeed, the 7 Principles and 7 core subjects are integral to

26000 (including the 7 core questions and the 7 principles any CSR approach. Moreover, it is more educative, func-

of Corporate Social Responsibility). tional and pragmatic to have access to an analysis grid

whose input sections are based on elements that shape

The 7 Principles and 7 core subjects of CSR established the organisation’s operations, enabling us to see how it

by ISO 26000 are not sub-criteria of AFAQ 26000 as such. integrates the principles and core subjects (at both strate-

They are integrated throughout the assessment model, gic and daily operational levels).

Sub-criteria Examples of points to be addressed

1.1. Global CSR reflection as the organisation-reflected on the contribution of its business

H

The organisation reflects comprehensively on to sustainable development: intrinsically? Through identifying all

the contribution of its business to sustainable its externalities?

development. s there within the organisation a clear reflection on how

I

Corporate Social Responsibility relates to the heart of its

business, not only today but also tomorrow?

hat is the scope of these reflections (people, activities,

W

processes...)?

1.2 Dialogue with stakeholders as the organisation identified all its stakeholders: both near and

H

The organisation identifies its stakeholders far, institutional and private individuals?

and dialogues with them to identify their s it able to understand their expectations in terms of sustainable

I

interests with regard to sustainable development and all of its own activities?

development.

o what extent does the organisation work in partnership with

T

its stakeholders to identify their expectations over time, their

interests and win/win strategies that can be developed?

1.3 Identification of sphere of influence as the organisation identified those of its stakeholders who

H

The organisation identifies, among all its constitute its sphere of influence (i.e. those that it has the

stakeholders, those who constitute its sphere capacity to influence in order to promote corporate social

of influence. responsibility and sustainable development practices)?

as the organisation identified, within its sphere of influence,

H

organisations or particular leaders who can convey the values

and practices of social responsibility?

ow is it organised so as to use this influence in the service

H

of sustainable development?

12 Assessment Guide AFAQ 26000 - Enterprises / Organizations

© Any integral or partial reproduction, made apart from an authorization express of AFNOR Certification or of its having causes, is illicit.

13. 1.4 Analysis of core subjects the challenges, risks and opportunities identified by the

Do

The organisation analyses the implications organisation comprehensively cover the 7 Core subjects of ISO

of the seven core subjects of ISO 26000 26000?

and related action areas for all its activities. analysing the implications of the core subjects for its activities

In

The 7 core subjects are: governance of the (and vice versa), does the organisation clearly identify all possible

organisation - human rights - labour relations

impacts (especially negative)?

and conditions - environment, - fair practices

- consumer issues - development and local the organisation able to specify, in relation to each core

Is

communities. subject, those CSR practices it is deploying and/or could or

should deploy?

1.5 Prioritisation of issues connection with sub-criterion 1.4 above, is the organisation

In

Has the organisation prioritised its issues able to prioritise, in order of importance, its different CSR issues

in terms of CSR, based on the seven core (constraints, opportunities, impacts, risks)?

subjects and dialogue with its stakeholders?

Are the issues identified as (significant) priorities not deadlocked

on issues related to one of the core subjects?

the issues identified as (significant) priorities cover the main

Do

environmental, social and economic aspects in an appropriate

and balanced way?

1.6 Governance and decision-making

Does the organisation follow transparent decision-making

The decision making processes of a business processes vis-à-vis internal stakeholders? External stakeholders?

include transparency, ethical behaviour,

Does the governance and decision-making of the organisation

respect for stakeholder interests and the take the interests of stakeholders into account?

principle of legality. They also include due

diligence concerning CSR actions.

Does the organisation, in its governance and decision-making

methods, incorporate monitoring for sustainable development,

stakeholder interests and points of vigilance concerning its CSR

activities?

1.7 Fair practices Has the organisation identified risks associated with its activities

The organisation conducts itself ethically in in terms of ethical conduct and fair practices (cartels, corruption,

its dealings with its stakeholders (business unfair non-competitive clauses, non-compliance with procurement

practices...). rules, misinformation on prices and or products, abuse of power

Fair practices include fair competition, vis-à-vis suppliers, partners, etc.)?

promotion of CSR, due diligence, prevention Does the organisation have prevention and/or monitoring

of complicity and the fight against corruption. practices and/or tools that ensure the fairness of its conduct in the

implementation of its activities?

Is the organisation proactive in the detection of risks and the

implementation of appropriate practices, internally and within its

sphere of influence?

1.8 Vision et Leadership With regard to the above questions, how do managers define

The leaders implement and share with the leadership and they share their vision, and what are the inputs?

entire organisation, and their sphere of How do leaders communicate their vision throughout the

influence, their vision of what CSR means organisation? Does this include a stance on the organisation’s

in terms of the core business missions. contribution to the global sustainable development issues? How

They demonstrate leadership based on the

are managers implementing their vision?

7 principles of ISO 26000. The 7 principles

are: -Accountability - Transparency - Ethical How do managers communicate their vision to their sphere of

Behaviour - Recognition of stakeholder influence? To what extent do they show leadership on the principles

interests, - Respect for the principle of of Corporate Social Responsibility?

legality - Incorporation of international

standards of behaviour - Respect for human

rights.

Assessment Guide AFAQ 26000 - Enterprises / Organizations 13

© Any integral or partial reproduction, made apart from an authorization express of AFNOR Certification or of its having causes, is illicit.

14. Human Environmental

AFAQ Production

and consumer

Resources

results

26000

Regional

protection

roots

Social

CORPORATE SOCIAL Strategy and results

corporate

RESPONSIBILITY Approach social

responsibility

Economic

results

Criterion 2 Implementation: Integration and communication of CSR

This section involves analysing how CSR strategy (and/ development principles into action in everyday business

or related policy/policies ) is supported by processes life.

(formal or otherwise) that enable its effective deployment The evaluator determines whether the integration of

within the company, in particular in order to achieve the sustainable development principles concerns all activi-

related objectives. ties/all business processes, with a view to continuous

This criterion involves assessing how the organisation’s improvement.

management can turn the integration of sustainable

Sub-criteria Examples of points to be addressed

2.1 Identification of strategies ow does the organisation’s strategy integrate its specific CSR issues?

H

Strategy, incorporating the main issues s this strategy expressed through the organisation’s activities,

I

of CSR, is translated into policies and including through policies that integrate its elements?

objectives. o the organisation’s strategy and policies incorporate objectives

D

relating to its Corporate Social Responsibility?

2.2 Identification of responsibilities s the organisation (identification of roles, missions, responsibilities) of

I

A clear organisation is defined and staff the entity clearly defined?

are enabled to deploy the CSR strategy oes such organisation provide for the deployment of CSR strategy

D

and policy. within the entity?

oes such organisation genuinely enable employees to effectively

D

deploy the strategy?

2.3 Integration of CSR ow does the organisation ensure the inclusion of Corporate Social

H

The organisation continuously improves Responsibility issues in all its practices, procedures, systems and

the integration of CSR in its practices, activities? To this end, how does it identify the various interfaces with

procedures, systems and activities. its stakeholders?

s the integration of CSR subject to continuous improvement, in terms

I

of improved practices and extension of scope?

oes the organisation assess the integration of CSR in its activities for

D

improvement purposes (through monitoring, indicators, information

systems...)?

2.4 Regulatory monitoring oes the organisation conduct regulatory monitoring?

D

The organisation conducts regulatory o what extent is this regulatory monitoring proactive (able to anticipate

T

monitoring and ensures its implementation. changes)?

ow does the organisation ensure the inclusion and sharing of data in

H

regulatory monitoring?

2.5 Monitoring of technological and oes the organisation monitor technological, competitive and best

D

competitive and best practices practices?

The organisation keeps track of the o what extent is this monitoring of market developments and practices

T

(technological and competitive) market and proactive (able to anticipate changes)?

monitors CSR practices carefully. ow does the organisation ensure the inclusion and sharing of data

H

from the monitoring of technological, competitive and best practices?

14 Assessment Guide AFAQ 26000 - Enterprises / Organizations

© Any integral or partial reproduction, made apart from an authorization express of AFNOR Certification or of its having causes, is illicit.

15. 2.6 Data and information oes the organisation analyse information and data on products,

D

management activities and/or the system?

Information and data on products, hat are the areas and limits of information and data involved and their

W

activities and/or the system is analysed links with corporate social responsibility issues?

and exploited. hat governance is provided by the organisation to analyse such

W

information and data (possible openness to external stakeholders)?

2.7 Internal communication ow does the organisation define the content of internal

H

Internal communication (vertical, horizontal communication as well as its targets?

and cross-cutting) facilitates the sharing of oes internal communication appropriately integrate the organisation’s

D

information. CSR issues?

hat are the internal communication procedures and do they allow

W

for the sharing of information in vertical, horizontal and cross-cutting

ways?

2.8 External communication ow does the organisation define the content of external

H

External communication facilitats communication as well as its targets?

appropriately and timely responses to the oes the external communication appropriately include the

D

information needs of stakeholders. organisation’s CSR issues?

hat are the external communication procedures and do these

W

(materials, vehicles, media...) enable stakeholders to be appropriately

informed and given an opportunity for dialogue?

Assessment Guide AFAQ 26000 - Enterprises / Organizations 15

© Any integral or partial reproduction, made apart from an authorization express of AFNOR Certification or of its having causes, is illicit.

16. Human Environmental

AFAQ Production

and consumer

Resources

results

26000

Regional

protection

roots

Social

CORPORATE SOCIAL Strategy and results

corporate

RESPONSIBILITY Approach social

responsibility

Economic

results

Criterion 3 Human resources, labour relations and practices

Better human resource management in the service of management skills, commitment, acknowledgement and

corporate strategy and improved implementation of the well-being of staff, not to mention labour relations.

actions to motivate men and women are core aspects Assessment should help to highlight these from a CSR

of business success. Corporate Social Responsibility perspective. Aspects of (physical but also mental) health

places men and women at the centre of its concerns and and safety are of course core concerns.

also acknowledges that the deployment of responsible

practices is in turn dependent on their involvement.

Human resource management practices clearly include

Sub-criterion Examples of points to be addressed

3.1 Human Resources and CSR re the organisation’s HR forecasts and plans consistent with its CSR

A

strategy. strategy?

HR-based forecasts and plans ensure hat are the links between CSR and HR within the organisation? Are

W

a fit between the organisation’s human these links the subject of an internal dialogue with employees and other

resources and its strategy. relevant stakeholders?

re these HR forecasts and plans, in line with CSR strategy, proactive

A

where necessary in terms of identifying new skills (internal/external...)

for recruitment or redeployment?

3.2 Training and skills oes the organisation ensure the awareness-raising/training of

D

Training and skills development on the employees regarding sustainable development and general principles

general principles of CSR and its impact of CSR?

on the company are offered to employees. oes the organisation ensure the awareness-raising /training of

D

employees regarding specific CSR issues?

oes the organisation ensure, where necessary, the training and

D

skills development employees regarding responses to specific HR

challenges?

3.3 Involvement of staff vis-à-vis CSR oes the organisation ensure employees are made aware of their

D

strategy impact on CSR issues within the organisation?

Staff are involved, accountable, and oes the organisation ensure the involvement and commitment of

D

acknowledged vis-à-vis achieving VSR staff vis-à-vis the achievement of CSR objectives? Are the relevant

goals. mechanisms sustainable?

re the staff accountable and acknowledged vis-à-vis the goals of

A

CSR?

3.4 Management of HR in line with the oes the organisation ensure respect for human rights and equity in its

D

principles of CSR human resource management and take account of cultural and social

Human resources management takes diversities?

account of cultural and social diversity and oes the organisation apply the principles of Corporate Social

D

respects equity and human rights at all Responsibility to its human resource management?

levels. s the implementation of human resource management based on CSR

I

principles supported by internal participatory approaches involving

staff?

3.5 Motivation and HR development ow does the organisation ensure the motivation and acknowledgment

H

Human resources management enables of its employees?

the motivation and recognition of staff as hat mechanisms facilitate skills and career development?

W

well as skills and career development. oes the organisation ensure a fit between such mechanisms and

D

employees’ expectations and needs?

16 Assessment Guide AFAQ 26000 - Enterprises / Organizations

© Any integral or partial reproduction, made apart from an authorization express of AFNOR Certification or of its having causes, is illicit.

17. 3.6 Labour dialogue hat are the labour dialogue procedures (consultation, cooperation,

W

Labour dialogue is based on discussions dialogue...) within the organisation?

with representative bodies and developed hat are the key issues in labour dialogue within the organisation?

W

through employer-employee consultation. o what extent do the organisation and its leaders promote labour

T

dialogue within the organisation?

3.7 Management of health and safety hat are the input data (diagnosis) of the organisation’s Health

W

at work Safety (HS) policy? What were the processes (contribution of

The organisation manages aspects of stakeholders...) followed in defining this policy?

health and safety, including risk prevention, hat fields are covered by the HS policy (physical safety, physical and

W

in partnership with all employees and mental stress, psychosocial problems...)?

those involved in its activities. hat is the scope of the organisation’s HS policy (sites, activities,

W

people, employees, external operators...)?

3.8 Labour conditions and relations hat are the input data (analysis, diagnosis, dialogue...) for the

W

The organisation ensures that all organisation’s reflection on working conditions in the broad sense?

employees, and persons involved in its hat topics are covered by the policies, practices and mechanisms

W

activities enjoy good working conditions, promoting good working conditions for employees? Are these subjects

particularly in terms of pay, hours and consistent with the challenges of the organisation’s role?

work/life balance and individuals’ hat are the policies, practices, devices, designed to create a healthy

W

relationship to their work. work/life balance?

Assessment Guide AFAQ 26000 - Enterprises / Organizations 17

© Any integral or partial reproduction, made apart from an authorization express of AFNOR Certification or of its having causes, is illicit.

18. Human Environmental

AFAQ Production

and consumer

Resources

results

26000

Regional

protection

roots

Social

CORPORATE SOCIAL Strategy and results

corporate

RESPONSIBILITY Approach social

responsibility

Economic

results

Criterion 4 Modes of production, consumption and consumer issues

This is one of the major aspects of sustainable devel- The organisation must analyse its use of such goods in

opment. Indeed, a company’s integration of sustainable particular, and possibly the competitive nature of this

principles is necessarily closely linked to two fundamen- deployment in terms of other users and interests.

tal factors: first, its area of activity (and its modes of pro- The perennial (sustainable) character or otherwise of

duction and consumption) and second, its geographical these goods must be the focus of this reflection, accom-

location(s), (considered below in terms of local integra- panied by an analysis of measures for conservation, sav-

tion and contribution to local development). ing, compensation, etc. that the organisation may wish

Sustainable development poses challenges for a number to consider.

of sectors making the transition from a «consumer econ- The evaluator analyses the consistency and depth of

omy» to a «service economy». the organisation’s CSR approach by evaluating the rel-

An ethical stance must be taken by the organisation on evance of its practices in terms of sustainable produc-

all issues, particularly in its relationship with and provi- tion and consumption.

sion of information to consumers and in protecting their

rights. Finally, the organisation’s contribution to sustain-

able development also involves identifying what is meant

by Public Goods (including «Global Public Goods»).

Sub-criteria Examples of points to be addressed

4.1 Innovation and design towards ow does the organisation incorporate sustainable development

H

sustainable production principles and issues into its innovation and design processes? Does

The organisation conducts an analysis of the organisation integrate these elements throughout the value chain

the life cycle of its products in its design and life cycle?

and innovation processes (eco-social oes the organisation integrate the relevant stakeholders in the stages

D

design). of innovation and design?

oes the organisation ensure the sharing of concerns and practices of

D

eco-social design among all staff involved in the stages of innovation

and design?

4.2 Purchase and selection of oes the organisation factor in the principles and issues of sustainable

D

products and services development in its choice of solutions and purchase of products and

The organisation manages its selection services?

of products and/or services and benefits, re the principles and issues of sustainable development incorporated

A

in connection with production and R into specifications for the purchase of products and services?

D, integrating social and environmental oes the organisation ensure the sharing of concerns and practices in

D

criteria in its specifications. terms of sustainable development among all employees involved in the

phases of selection and purchase of products and services?

4.3 Purchasing and supplier oes the organisation factor in the principles and issues of sustainable

D

relationships development into in its choice of suppliers and providers?

The organisation manages its choice re the principles and issues of sustainable development integrated

A

of suppliers and its relations with them into tools for analysis, assessment and/or recognition in the choice of

in promoting CSR throughout the value suppliers and providers?

chain. oes the organisation ensure the sharing of concerns and practices in

D

terms of sustainable development among all employees involved in the

selection of suppliers and service providers?

18 Assessment Guide AFAQ 26000 - Enterprises / Organizations

© Any integral or partial reproduction, made apart from an authorization express of AFNOR Certification or of its having causes, is illicit.